Country

Companies10 of 11

mambu.com

Mambu

mambu.com🇩🇪 Germany

Mambu is a cloud-native banking software platform that lets financial institutions and fintechs launch and operate lending and deposit products without building from scratch. Rather than forcing customers into rigid legacy systems, Mambu provides composable banking infrastructure—modular APIs and pre-built components that work together or stand alone, depending on what you actually need.

The company sits at the intersection of two fintech realities: traditional banks are drowning in outdated core systems that can't keep pace with market demands, while new lenders and neobanks need speed without sacrificing compliance or scale. Mambu's approach is to be the operating system underneath, handling the heavy lifting of loan origination, deposit management, portfolio servicing, and regulatory reporting while letting clients focus on customer experience and product innovation.

What makes Mambu different from other core banking platforms is its emphasis on velocity. Institutions deploy in weeks rather than years. The platform is genuinely modular—you can pick the lending module, the deposit module, or both, and layer in third-party services through APIs. This flexibility has resonated with everyone from African microfinance networks to European challenger banks to enterprise lenders managing complex credit products.

Mambu is now a critical piece of infrastructure in the emerging markets fintech ecosystem, particularly across Africa and Asia, where it powers lending operations for hundreds of financial institutions. In Europe, it's carved out space among mid-market and challenger banks looking to avoid the capital expenditure and technical debt of legacy systems. The company represents a broader shift in fintech: away from end-to-end platforms that claim to do everything, toward specialized infrastructure that does one thing—backend financial operations—exceptionally well.

Categories

LendingDigital BankingFinancial Infrastructure

0

upvotes

ebury.com

Ebury

ebury.com🇬🇧 United Kingdom

Ebury is a fintech platform that helps small and medium-sized businesses manage their international payments and foreign exchange exposure. Founded in 2009, the company has grown into a significant player in cross-border commerce, serving thousands of SMEs across Europe and beyond who need to move money across currencies without the friction and cost of traditional banking.

The platform combines payment processing, FX services, and working capital financing into a single interface. Rather than juggling multiple bank relationships and struggling with opaque exchange rates, businesses get transparent pricing, competitive rates, and a digital-first experience that actually reflects how modern commerce operates. Ebury handles the complexity of international payments—whether that's paying suppliers in Poland, collecting revenue in Singapore, or managing exposure across dozens of currencies.

What sets Ebury apart in a crowded market is its focus on the unglamorous but essential problem of trade finance for SMEs. While fintechs chase consumer banking or headline-grabbing crypto plays, Ebury has quietly become indispensable to thousands of businesses that simply need reliable, cost-effective cross-border infrastructure. The company has expanded beyond payments into working capital solutions, recognizing that businesses moving money internationally often need flexible financing alongside their payment rails.

Ebury represents a pragmatic slice of European fintech—solving real problems for real businesses, generating sustainable revenue, and building the kind of B2B financial infrastructure that underpins European commerce.

Categories

PaymentsSME FinanceLendingTreasury

0

upvotes

younited-credit.com

Younited Credit

younited-credit.com🇫🇷 France

Younited Credit sits at the intersection of consumer lending and fintech, offering personal loans to borrowers across Europe who want speed and transparency instead of the bureaucratic friction of traditional banks. Founded in 2011, the company has evolved from a peer-to-peer lending marketplace into a full-stack credit platform that sources, prices, and services loans for both retail customers and institutional partners.

The core product is straightforward: quick online approval (often minutes), competitive rates based on real underwriting, and a streamlined digital experience that feels more like ordering something on your phone than sitting in a bank branch. What distinguishes Younited from the crowded European consumer lending space is its scale and sophistication. Rather than just operating a marketplace, the company has built proprietary credit scoring models, automated servicing infrastructure, and a diversified funding model that includes institutional investors, warehouse financing, and securitization. This means Younited isn't dependent on peer-to-peer investors or a single funding source—it can grow independently. The platform operates across multiple European markets and has become a quiet infrastructure player for consumer credit, processing loans for direct borrowers while also powering lending for third parties through white-label partnerships. In an era when legacy banks still treat personal lending like a commodity and fintechs are scrambling to prove unit economics, Younited represents the pragmatic middle ground: technology-first underwriting and customer experience wrapped around a business model that actually scales profitably.

Categories

LendingPersonal Finance

0

upvotes

zopa.com

Zopa

zopa.com🇬🇧 United Kingdom

Zopa is one of Europe's longest-running peer-to-peer lending platforms, though it's evolved well beyond that origin story. What started as a way to connect borrowers and savers directly has matured into a more sophisticated consumer credit player that combines traditional lending infrastructure with a distinctly digital-first approach. The company now operates across unsecured personal loans, credit products, and a growing fintech ecosystem that blends borrowing, saving, and investing.

At its core, Zopa sits at the intersection of traditional consumer finance and fintech disruption. It's not a bank trying to be digital, nor is it a pure lending marketplace anymore—it's something closer to a modern credit platform that understands both the mechanics of real lending and the UX expectations of digital natives. The platform uses data and technology to assess creditworthiness in ways that older lenders rarely do, and it's built a customer base that appreciates transparency in borrowing costs.

In the European consumer lending landscape, Zopa occupies a unique position. It arrived earlier than most, which has given it brand recognition that newer competitors still lack, but also the burden of evolution—moving from a community-driven marketplace model to a more scalable, institutional lending model. Unlike many fintech lenders that chase rapid growth through aggressive marketing, Zopa has maintained a reputation for responsible lending and clear communication, which appeals to the thoughtful borrower rather than the desperate one.

Today, Zopa represents a maturing segment of fintech: the lesson that technology alone doesn't guarantee success, but technology paired with operational discipline and regulatory responsibility does. It's a blueprint for how a 2005-era fintech idea can actually sustain and scale in 2024.

Categories

LendingPersonal Finance

0

upvotes

auxmoney.com

auxmoney

auxmoney.com🇩🇪 Germany

auxmoney sits at the intersection of peer-to-peer lending and digital financial inclusion. The Berlin-based platform connects individual investors with borrowers seeking personal loans, sidestepping traditional bank gatekeeping through algorithmic credit assessment and a streamlined approval process.

Since 2007, it has built one of Europe's more mature alternative lending marketplaces, processing billions in credit and establishing itself as a credible counterweight to institutional finance for everyday lending needs. What sets auxmoney apart in the crowded P2P lending space is its focus on accessibility: borrowers who might struggle with conventional bank criteria can access capital, while investors gain exposure to diversified consumer credit without the friction of direct lending management. The platform automates origination, servicing, and investor payouts, handling the operational complexity that keeps most people out of direct lending. auxmoney doesn't pretend to be a bank—it's unapologetically a marketplace, transparent about risk and returns in ways traditional lenders rarely are.

In a European fintech landscape increasingly dominated by neobanks and payment startups, auxmoney represents a quieter but steadier category: the infrastructure that lets capital find borrowers efficiently. Its longevity and scale demonstrate that P2P lending, despite early hype and inevitable casualties, has become infrastructure for people and investors outside the conventional banking circle.

Categories

Lending

0

upvotes

inbank.eu

Inbank

inbank.eu🇪🇪 Estonia

Inbank is a Baltic-born digital lending platform that treats credit scoring like a science rather than an art. Founded in 2016, it's built a reputation for getting to yes faster than traditional lenders, using alternative data and machine learning to assess borrowers who might otherwise fall through the cracks. The company operates across multiple European markets, offering everything from consumer loans to invoice financing, all wrapped in a slick mobile interface that makes borrowing feel less bureaucratic.

What sets Inbank apart is its obsession with speed and transparency. Where legacy banks demand weeks of paperwork, Inbank delivers decisions in minutes. It's also not afraid to lend to people without perfect credit histories—the platform's algorithms look beyond traditional metrics to spot reliable borrowers. The company has positioned itself as the bridge between underserved consumers and institutional capital, working with banks, insurance companies, and other financial players to distribute credit more efficiently.

In the European fintech landscape, Inbank occupies a rare middle ground: it's scaled across multiple countries without losing its agility, and it's mastered both direct-to-consumer lending and B2B partnerships. Rather than fighting incumbents head-on, it's become the infrastructure that helps traditional finance lend smarter. That positioning—as a trusted technology partner rather than a disruptor—has kept it stable through multiple market cycles and regulatory shifts.

Categories

LendingEmbedded Finance

0

upvotes

wayflyer.com

Wayflyer

wayflyer.com🇮🇪 Ireland

Wayflyer is an Irish fintech that solves a peculiar problem in e-commerce: founders who sell online often can't access the capital they need because traditional banks don't understand their business model. The company uses real-time sales data from platforms like Shopify and Amazon to underwrite credit decisions in minutes rather than months, offering flexible funding with repayment terms tied directly to daily revenue.

What makes Wayflyer different is its willingness to lend to merchants that legacy finance overlooks—lower-revenue sellers, newer businesses, international operators. While traditional lenders fixate on collateral and personal credit scores, Wayflyer looks at transaction flows, growth trajectory, and actual business performance. The underwriting is algorithmic, the approval is fast, and the cost is transparent. You don't need perfect credit or three years of accounts. You need sales data.

In the crowded world of e-commerce financing, most players focus either on micro-loans or venture-scale rounds. Wayflyer operates in the messy middle—typically funding between €5,000 and €500,000 for merchants generating €30,000+ monthly revenue. It competes with Shopify Capital in North America but has built particular strength across Europe, where merchant fragmentation is higher and credit access more constrained.

The company represents a broader shift in fintech: away from point solutions toward platforms that integrate data, credit decisioning, and cash flow management. Wayflyer isn't just lending; it's becoming infrastructure for the digital commerce economy, particularly for the thousands of small sellers who power e-commerce but remain invisible to traditional finance.

Categories

LendingSME Finance

0

upvotes

bidfinance.eu

Bid Finance

bidfinance.eu🇵🇱 Poland

Bid Finance is a European platform that streamlines how small and mid-sized businesses access working capital finance. Rather than the traditional dance of chasing multiple lenders and dealing with weeks of paperwork, the platform lets SMEs connect with a curated network of funding providers—banks, alternative lenders, and institutional investors—through a single application. The process is built around speed and transparency: once a business posts its financing need, multiple lenders can compete for the deal, which typically means better terms and faster decisions.

What sets Bid Finance apart is its marketplace model. Instead of being another loan originator or broker that simply refers you somewhere else, it facilitates genuine competition between funders. SMEs see real-time offers and can compare pricing and terms side by side. It's the B2B equivalent of price transparency in consumer finance, but applied to the murky world of business lending where information asymmetry has long been the norm.

The platform operates across multiple European markets, positioning itself as a pan-European solution for working capital, invoice financing, and asset-based lending. It targets businesses that don't fit neatly into the big bank's playbooks—growing firms that need flexible, responsive funding without the bureaucracy. For lenders, it reduces sourcing costs and lets them plug into deal flow they'd otherwise struggle to access.

Bid Finance represents a broader shift in how European SMEs access capital: moving away from relationship banking and towards digital-first, competitive marketplaces where multiple parties bid on deals in near real-time.

Categories

LendingSME Finance

0

upvotes

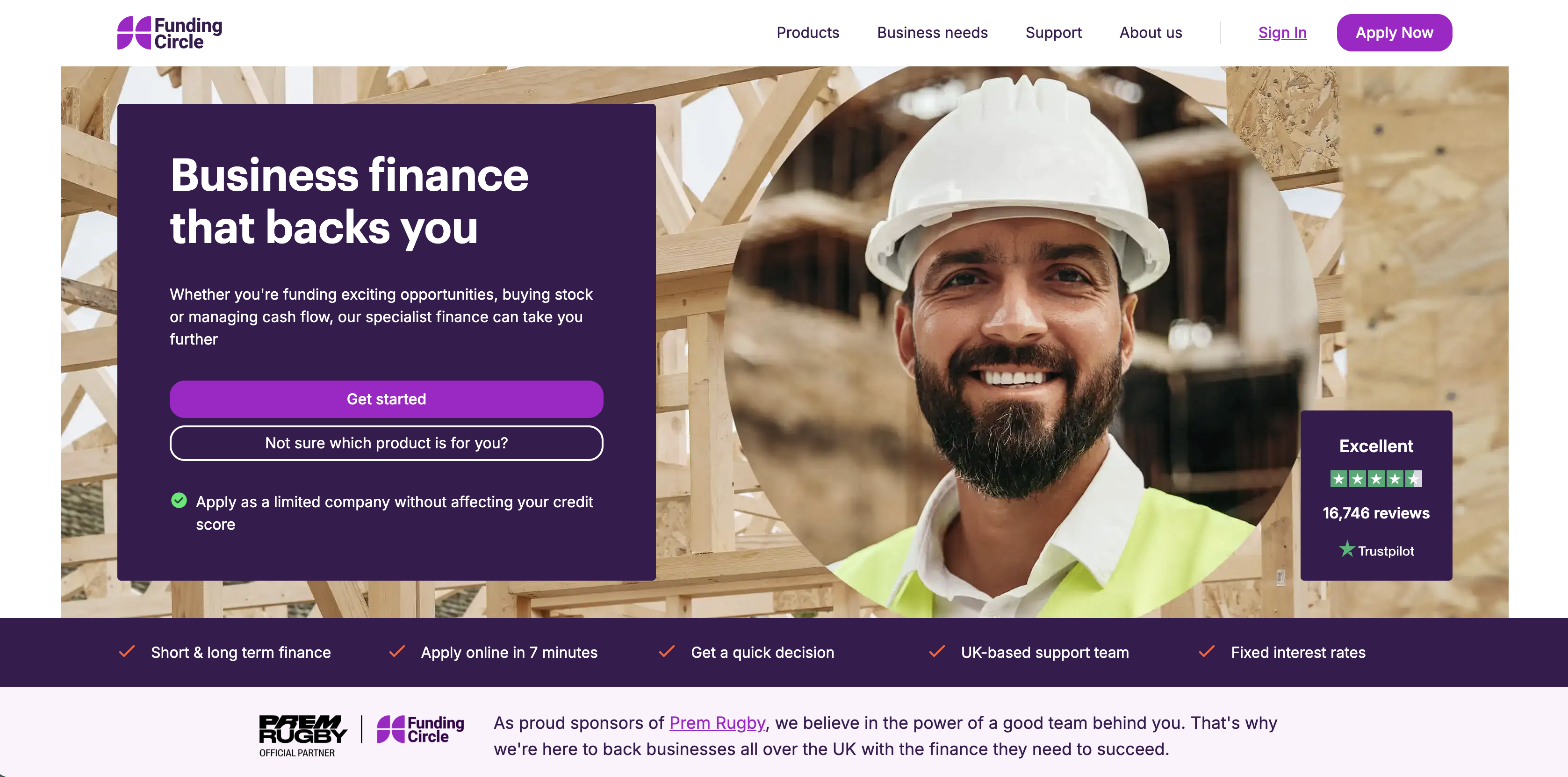

fundingcircle.com

Funding Circle

fundingcircle.com🇬🇧 United Kingdom

Funding Circle sits at the intersection of institutional capital and small business ambition. The platform connects SMEs with investors—funds, banks, and individuals—who want returns tied to real economic activity rather than abstract asset classes. It's fundamentally a marketplace, but one that's spent years learning how to assess credit risk at scale, price loans competitively, and move money across borders without the friction traditional finance demands.

The company operates across multiple geographies, though Europe remains central to its strategy. It handles everything from loan origination and underwriting through to servicing and portfolio management, meaning it's built real infrastructure rather than just matching borrowers to lenders. This matters because it allows institutional investors to actually understand what they're funding.

Funding Circle competes in a space where traditional banks have historically been absent—the mid-market lending gap where a £50,000 loan isn't big enough for a relationship manager but too important for a business to ignore. Alternative lenders have crowded this space, but Funding Circle's institutional backing and regulatory maturity give it a structural advantage. It's moved from pure peer-to-peer model toward a more hybrid approach, partnering with regulated lenders to expand reach while maintaining its marketplace credibility.

The company represents a fundamental rethinking of how capital reaches productive SMEs—not through gatekeepers, but through platforms that make risk transparent and pricing efficient.

Categories

LendingSME Finance

0

upvotes

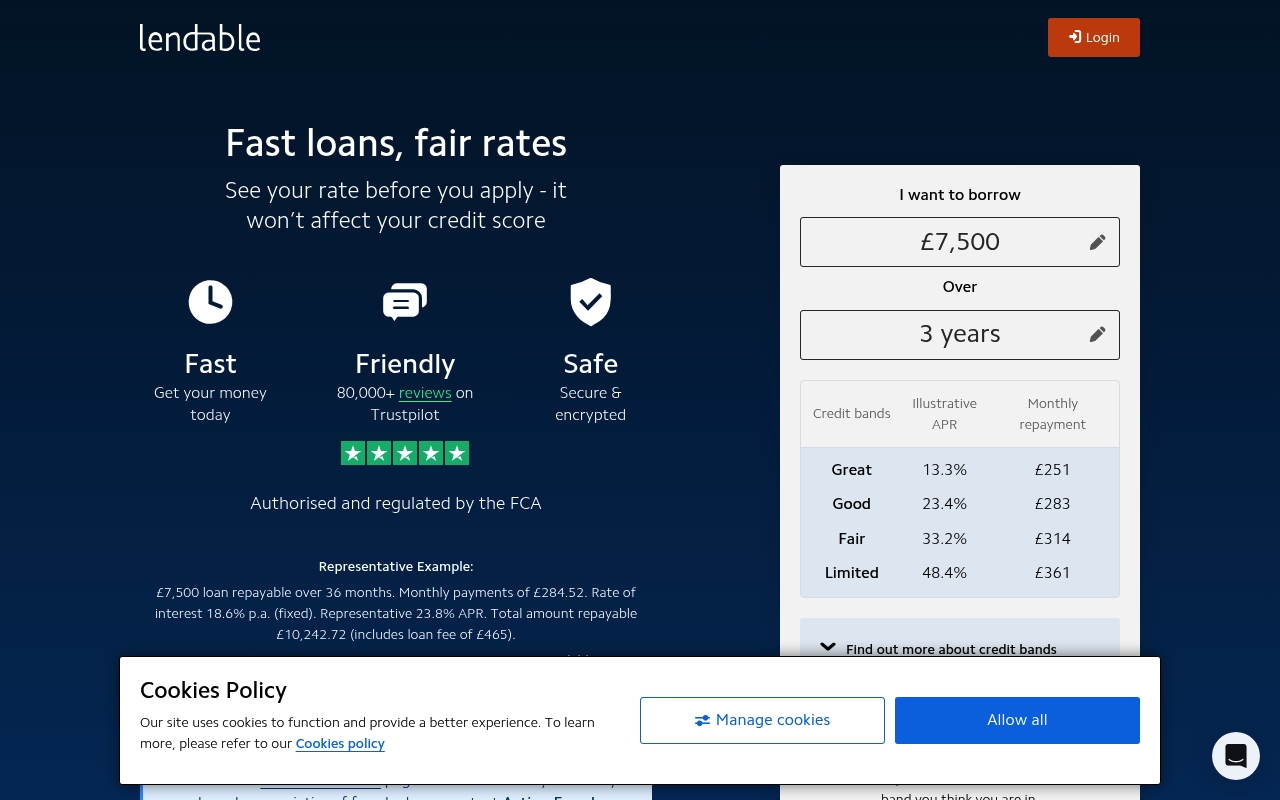

lendable.co.uk

Lendable

lendable.co.uk🇬🇧 United Kingdom

Lendable sits at the intersection of institutional finance and algorithmic credit. It's a platform that connects alternative lenders—think peer-to-peer platforms, fintechs, and non-bank lenders—with institutional capital markets. Rather than originating loans itself, Lendable acts as a market infrastructure layer, securitizing consumer and SME loan portfolios and selling them to institutional investors hungry for yield in an era of low rates.

The company essentially democratized access to capital markets for non-traditional lenders. Before Lendable, a mid-sized P2P lender or online SME lender couldn't easily tap into the deep-pocketed institutional buyers that banks routinely access. Lendable changed that by building the plumbing—origination APIs, portfolio management tools, and securitization infrastructure—that lets alternative lenders scale without warehousing risk on their own balance sheets.

In the European fintech landscape, Lendable represents a specific but growing category: the infrastructure play that enables other fintechs to thrive. It's not a consumer app; it's the backbone that lets consumer-facing lenders actually fund their ambitions. The platform has processed billions in loan assets and works with some of Europe's most recognizable fintech names.

Lendable's role in the broader ecosystem is that of a bridge—connecting the new world of distributed lending with the old world of institutional capital. It's quietly important infrastructure, the kind of thing that doesn't grab headlines but fundamentally reshapes how credit flows.

Categories

LendingFinancial InfrastructureCapital Markets

0

upvotes