Country

Companies2 of 2

tink.com

TinkFeatured

tink.com🇸🇪 Sweden

Tink is a Swedish open banking platform that connects to over 3,000 financial institutions across Europe, solving the friction between fintech ambition and banking reality. Rather than building their own infrastructure from scratch, startups and established financial companies plug into Tink's APIs to instantly access account data, initiate payments, and orchestrate complex financial workflows without dealing with legacy banking plumbing.

The company sits at the intersection of three powerful trends: the shift toward embedded finance, the regulatory tailwinds of PSD2 and Open Banking, and the growing irrelevance of traditional bank APIs. While competitors chase headlines with consumer-facing apps, Tink operates in the less glamorous but infinitely more valuable B2B2C layer—the infrastructure that quietly powers dozens of European fintech winners.

What sets Tink apart is execution at scale. Their data aggregation and payment initiation services work reliably across fragmented European banking systems, which is harder than it sounds. Most fintechs eventually realize they need a Tink-like layer to escape the nightmare of maintaining connections to hundreds of banks with different technical standards and frequent updates.

That importance hasn’t gone unnoticed. In 2022, Tink was acquired by Visa, a move that underscored just how critical open banking infrastructure has become. The acquisition gave Tink both validation and reach, positioning it even closer to the core of the global payments ecosystem.

Tink represents the unglamorous backbone of modern European fintech—the kind of company that doesn't dominate headlines but becomes quietly indispensable to everyone building financial products.

Categories

Open BankingFinancial InfrastructureEmbedded Finance

1

upvotes

klarna.com

Klarna

klarna.com🇸🇪 Sweden

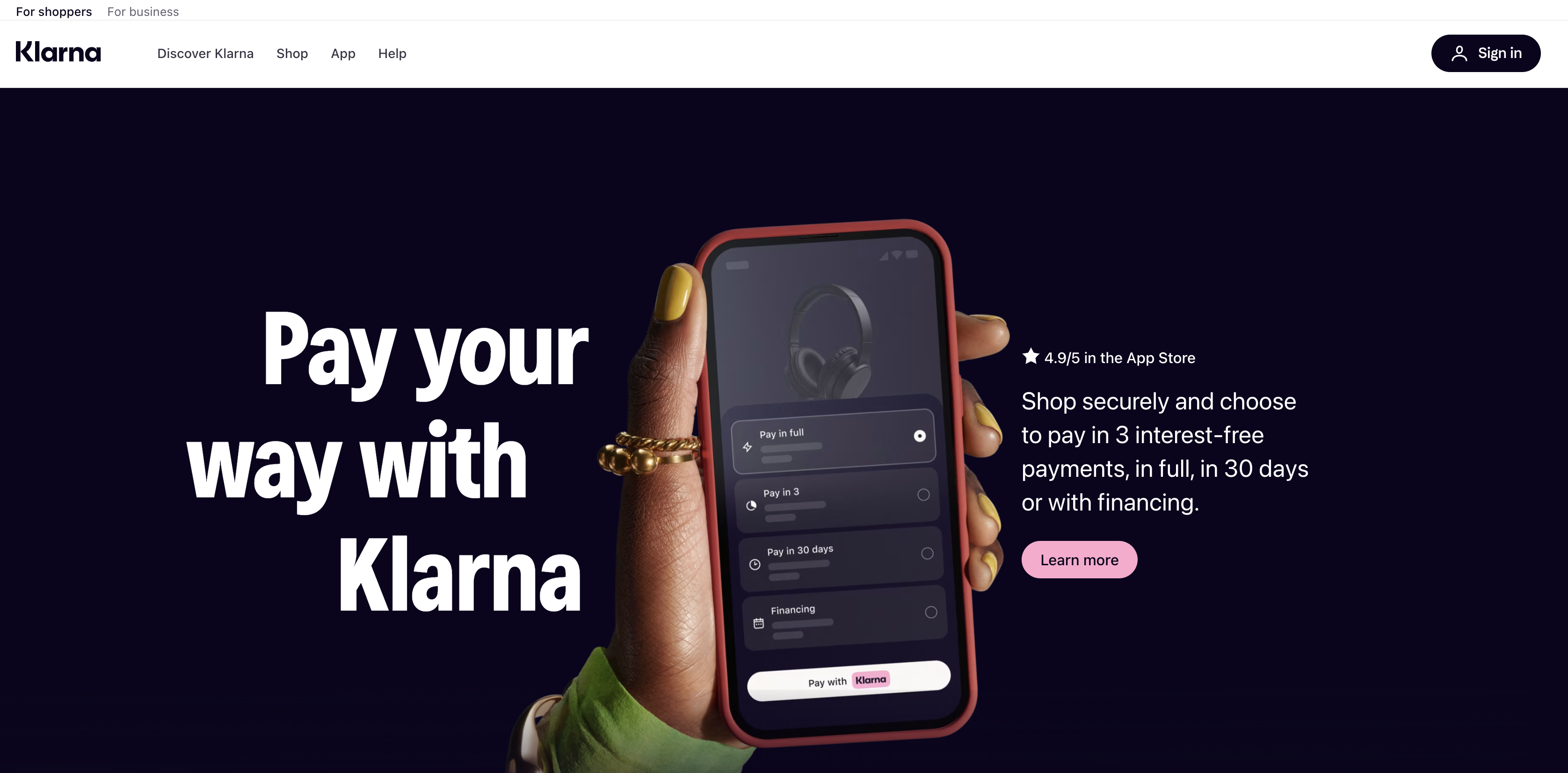

Klarna is the European fintech that made shopping on credit feel frictionless. It started by asking a simple question: why do you need a credit card to buy something online? The answer became a payments platform that lets consumers split purchases into instalments, skip the card altogether, and pay later—without the friction of traditional lending.

The company operates across three overlapping worlds: it's a checkout experience for shoppers, a payments infrastructure for merchants, and increasingly, a full-fledged bank. Consumers use the app to manage their finances across a growing ecosystem of partners, while retailers get a payment method that reduces cart abandonment and increases average order value. Behind the scenes, Klarna runs credit decisioning at scale, onboarding millions of users with minimal friction.

In a market crowded with BNPL competitors, Klarna stands out through sheer reach and merchant relationships. It's available at retailers ranging from Sephora to furniture chains across Europe, the US, and beyond. The company has moved well beyond point-of-sale lending—it now operates a full banking licence in some markets, offers savings accounts, and is building out wealth tools.

Klarna represents a broader shift in European fintech: the blurring of checkout, lending, and banking into a single consumer experience. It's become essential infrastructure for modern retail, reshaping how millions of people think about spending and borrowing.

Categories

BNPLPaymentsDigital BankingEmbedded Finance

0

upvotes