Country

Companies10 of 23

checkout.com

Checkout.com

checkout.com🇬🇧 United Kingdom

Checkout.com is a global payments infrastructure company that builds the plumbing beneath the surface of e-commerce. While most payment processors still operate like legacy banking rails, Checkout.com has constructed a single API that connects directly to card networks, acquiring banks, and alternative payment methods—eliminating the middlemen that slow everything down. The platform processes payments in over 150 currencies across 195 countries, handling everything from straightforward card transactions to complex multi-currency settlements for merchants operating at scale.

What sets it apart in Europe and beyond is its refusal to be a typical payment gateway: instead of asking merchants to adapt to the network, Checkout.com adapts the network to the merchant. Founded in 2012 by Guillermo Gutiérrez García-Ceballos, the company has grown from a London-based startup into a critical piece of infrastructure for enterprises, fintechs, and marketplaces that need orchestration at the transaction level. It competes with traditional acquirers and modern payment platforms by combining the reliability of legacy banking with the speed and flexibility developers expect.

In the fragmented European payments landscape, Checkout.com has become indispensable for companies that refuse to compromise on latency, coverage, or control. The company represents a fundamental shift in how payments should work: less about choosing between payment methods and more about making payments invisible.

Categories

PaymentsFinancial InfrastructureEmbedded Finance

0

upvotes

fundingcircle.com

Funding Circle

fundingcircle.com🇬🇧 United Kingdom

Funding Circle sits at the intersection of institutional capital and small business ambition. The platform connects SMEs with investors—funds, banks, and individuals—who want returns tied to real economic activity rather than abstract asset classes. It's fundamentally a marketplace, but one that's spent years learning how to assess credit risk at scale, price loans competitively, and move money across borders without the friction traditional finance demands.

The company operates across multiple geographies, though Europe remains central to its strategy. It handles everything from loan origination and underwriting through to servicing and portfolio management, meaning it's built real infrastructure rather than just matching borrowers to lenders. This matters because it allows institutional investors to actually understand what they're funding.

Funding Circle competes in a space where traditional banks have historically been absent—the mid-market lending gap where a £50,000 loan isn't big enough for a relationship manager but too important for a business to ignore. Alternative lenders have crowded this space, but Funding Circle's institutional backing and regulatory maturity give it a structural advantage. It's moved from pure peer-to-peer model toward a more hybrid approach, partnering with regulated lenders to expand reach while maintaining its marketplace credibility.

The company represents a fundamental rethinking of how capital reaches productive SMEs—not through gatekeepers, but through platforms that make risk transparent and pricing efficient.

Categories

LendingSME Finance

0

upvotes

bricklane.com

Bricklane

bricklane.com🇬🇧 United Kingdom

Bricklane is a London-based property management platform that strips away the friction from rental investing. The company handles everything from tenant screening and rent collection to maintenance coordination and compliance reporting, turning property ownership from a logistical nightmare into something actually manageable. Rather than juggling spreadsheets, emails, and contractors across multiple platforms, landlords and property managers get a unified dashboard with real-time insights into their portfolio.

What sets Bricklane apart in the increasingly crowded proptech space is its operational ruthlessness. While competitors get distracted by flashy features, Bricklane focuses relentlessly on the stuff that actually matters: making sure rent arrives on time, repairs get scheduled without a dozen phone calls, and the regulatory mountain of UK rental law stays manageable. The platform integrates with accounting software and mortgage lenders, which means less manual data entry and fewer reconciliation headaches.

The company sits at an interesting intersection of fintech and real estate infrastructure. It's not quite a lender, but it enables property financing by making the assets themselves easier to manage and therefore more attractive to institutional investors. For individual landlords drowning in admin, Bricklane represents a different kind of fintech: one that acknowledges property is less about disruption and more about efficiency. In the UK rental market, where compliance complexity and tenant friction are endemic, that focus on unglamorous operational excellence is genuinely radical.

Categories

Real Estate FinanceDigital Banking

0

upvotes

darktrace.com

Darktrace

darktrace.com🇬🇧 United Kingdom

Darktrace is a British artificial intelligence company that weaponizes self-learning algorithms against cyber threats in real-time. Founded in 2013 by mathematicians and former Cambridge scholars, it operates at the intersection of enterprise security and AI—teaching machines to recognize the fingerprint of normal behavior, then catching deviation before damage happens.

The platform works differently from traditional cybersecurity. Rather than relying on threat signatures or static rules, Darktrace's core AI engine learns what "normal" looks like inside an organization's network—every user, device, and data flow. When something deviates fundamentally from that baseline, it triggers. This approach has made it essential infrastructure for financial institutions, healthcare operators, and multinational enterprises handling sensitive data.

What separates Darktrace from older guard security providers is speed and scope. While competitors still operate on vulnerability lists and known-bad signatures, Darktrace catches unknown threats in motion. It's become the gold standard for enterprises that treat security as an ongoing conversation with AI, not a compliance checkbox.

In the broader fintech and enterprise tech landscape, Darktrace represents a generation of AI-native security companies that don't just react to attacks—they learn, predict, and evolve. For financial services and regulated industries, this autonomous intelligence has become non-negotiable.

Categories

Fraud & SecurityFinancial Infrastructure

0

upvotes

primarybid.com

Primary Bid

primarybid.com🇬🇧 United Kingdom

Primary Bid sits at the intersection of investment access and market fairness. For years, retail investors have watched from the sidelines while institutional players get first crack at hot IPO allocations. Primary Bid flips that script, letting everyday people invest in initial public offerings directly, cutting out the traditional gatekeepers that have hoarded these opportunities.

The platform operates as a digital intermediary between retail investors and companies going public, democratizing access to what was once a VIP-only event. It's not just about fairness—it's about giving ordinary Europeans the chance to participate in wealth creation at the most exciting moment in a company's lifecycle.

Unlike traditional investment banks that cherry-pick their favored clients, Primary Bid opens the IPO window to anyone with a UK brokerage account. This challenges the old model where your wealth determined your access. The company essentially rebuilds the IPO process for the internet age, stripping away exclusivity and replacing it with transparency and scale.

In the broader fintech landscape, Primary Bid represents a quiet but powerful shift toward democratized capital markets—proving that retail investors aren't just traders chasing memes, but serious participants worthy of institutional-quality opportunities.

Categories

Capital MarketsWealth

0

upvotes

monzo.com

Monzo

monzo.com🇬🇧 United Kingdom

Monzo is a mobile-first digital bank that has spent the last decade proving that banking doesn't need to feel like a relic from the 1980s. Built for smartphones rather than retrofitted onto them, the app strips away the friction of traditional banking—opening an account takes minutes, spending notifications arrive in real time, and money management happens where you're already looking: your phone.

The company operates as a fully licensed UK bank, not just a payments layer on top of someone else's infrastructure. That matters. It means Monzo holds deposits, offers overdrafts, issues physical and virtual debit cards, and increasingly functions as a complete financial home for a generation that never wanted a branch.

What separates Monzo from the neobank noise is its relentless focus on customer experience and transparency. There are no hidden fees, no complicated terms, and the company communicates directly with users through in-app messaging. Spending analytics happen automatically; budgeting tools surface insights without lectures. The interface is designed for people, not processes.

In the European fintech landscape, Monzo represents the mature challenger bank—no longer purely disruptive, but profitable and expanding. It's expanded beyond the UK into Europe, launched business accounts, and continues to add services like savings pots and financial wellness features. It's the answer to the question: what happens when a digital bank stops experimenting and starts becoming the primary financial account.

Categories

Digital BankingPersonal Finance

0

upvotes

starlingbank.com

Starling Bank

starlingbank.com🇬🇧 United Kingdom

Starling Bank is a British challenger bank that stripped away the friction of traditional banking and rebuilt it around what modern customers actually need: instant notifications, real-time spending insights, and accounts you can open in minutes without stepping into a branch. Founded in 2014, it operates as a fully regulated bank with its own banking license, not just a wrapper around legacy infrastructure.

The platform serves both consumers and SMEs, offering straightforward current accounts, savings pots, and increasingly sophisticated business banking tools. Unlike neobanks reliant on partnerships, Starling owns its core infrastructure, which means faster iteration and tighter product control. The company has built a reputation for no-nonsense transparency: no hidden fees, no overdraft tricks, and clear communication about what you're getting.

In the crowded UK digital banking space, Starling stands apart through consistent execution and a focus on solving real problems rather than chasing hype. It's profitable, self-sufficient, and treated by legacy banks as a genuine competitor rather than a novelty. For European fintechs, Starling represents the successful blueprint: regulated, capital-efficient, and genuinely preferred by millions of users who value simplicity over flashiness.

As the fintech landscape matures, Starling exemplifies the shift from disruption theater to sustainable banking infrastructure—a reminder that the most radical innovation often looks deceptively simple.

Categories

Digital BankingSME FinancePersonal Finance

0

upvotes

zopa.com

Zopa

zopa.com🇬🇧 United Kingdom

Zopa is one of Europe's longest-running peer-to-peer lending platforms, though it's evolved well beyond that origin story. What started as a way to connect borrowers and savers directly has matured into a more sophisticated consumer credit player that combines traditional lending infrastructure with a distinctly digital-first approach. The company now operates across unsecured personal loans, credit products, and a growing fintech ecosystem that blends borrowing, saving, and investing.

At its core, Zopa sits at the intersection of traditional consumer finance and fintech disruption. It's not a bank trying to be digital, nor is it a pure lending marketplace anymore—it's something closer to a modern credit platform that understands both the mechanics of real lending and the UX expectations of digital natives. The platform uses data and technology to assess creditworthiness in ways that older lenders rarely do, and it's built a customer base that appreciates transparency in borrowing costs.

In the European consumer lending landscape, Zopa occupies a unique position. It arrived earlier than most, which has given it brand recognition that newer competitors still lack, but also the burden of evolution—moving from a community-driven marketplace model to a more scalable, institutional lending model. Unlike many fintech lenders that chase rapid growth through aggressive marketing, Zopa has maintained a reputation for responsible lending and clear communication, which appeals to the thoughtful borrower rather than the desperate one.

Today, Zopa represents a maturing segment of fintech: the lesson that technology alone doesn't guarantee success, but technology paired with operational discipline and regulatory responsibility does. It's a blueprint for how a 2005-era fintech idea can actually sustain and scale in 2024.

Categories

LendingPersonal Finance

0

upvotes

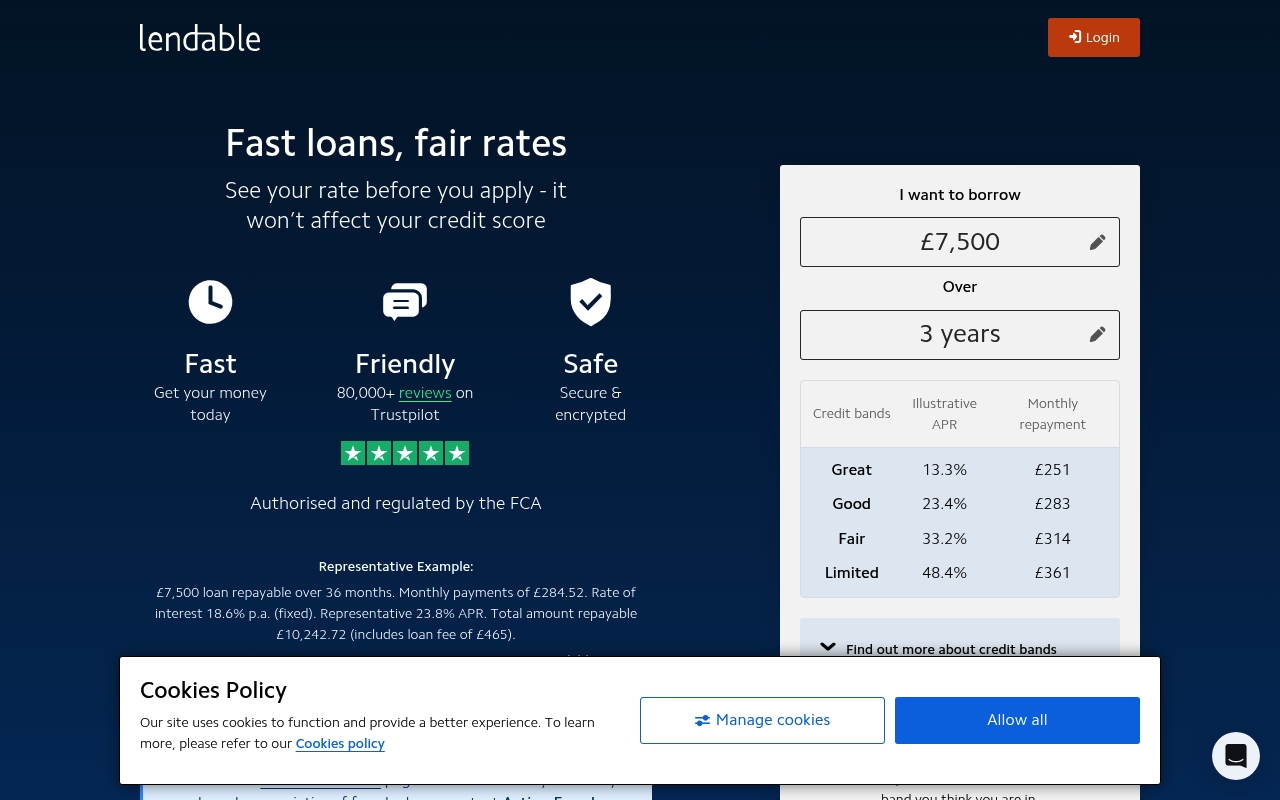

lendable.co.uk

Lendable

lendable.co.uk🇬🇧 United Kingdom

Lendable sits at the intersection of institutional finance and algorithmic credit. It's a platform that connects alternative lenders—think peer-to-peer platforms, fintechs, and non-bank lenders—with institutional capital markets. Rather than originating loans itself, Lendable acts as a market infrastructure layer, securitizing consumer and SME loan portfolios and selling them to institutional investors hungry for yield in an era of low rates.

The company essentially democratized access to capital markets for non-traditional lenders. Before Lendable, a mid-sized P2P lender or online SME lender couldn't easily tap into the deep-pocketed institutional buyers that banks routinely access. Lendable changed that by building the plumbing—origination APIs, portfolio management tools, and securitization infrastructure—that lets alternative lenders scale without warehousing risk on their own balance sheets.

In the European fintech landscape, Lendable represents a specific but growing category: the infrastructure play that enables other fintechs to thrive. It's not a consumer app; it's the backbone that lets consumer-facing lenders actually fund their ambitions. The platform has processed billions in loan assets and works with some of Europe's most recognizable fintech names.

Lendable's role in the broader ecosystem is that of a bridge—connecting the new world of distributed lending with the old world of institutional capital. It's quietly important infrastructure, the kind of thing that doesn't grab headlines but fundamentally reshapes how credit flows.

Categories

LendingFinancial InfrastructureCapital Markets

0

upvotes

freetrade.io

Freetrade

freetrade.io🇬🇧 United Kingdom

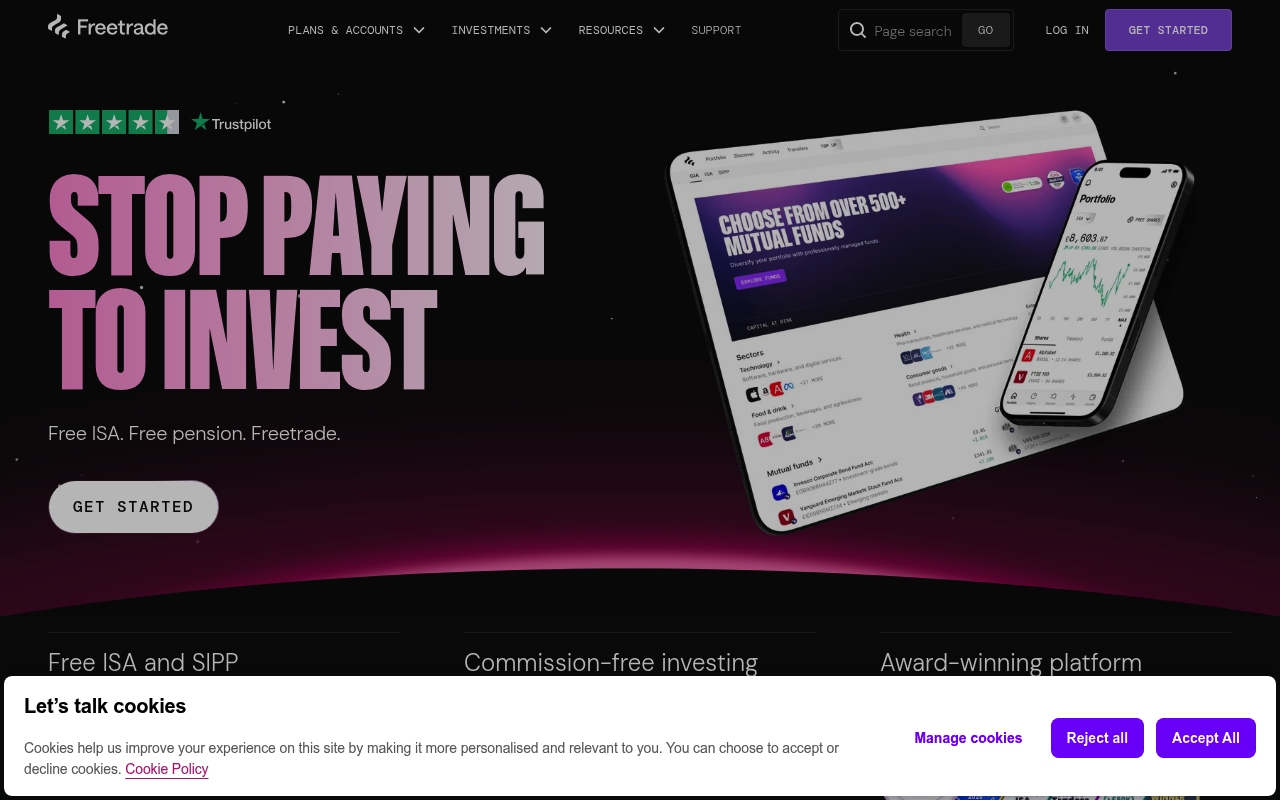

Freetrade is a London-based investing app that stripped away the gatekeepers between everyday Europeans and the stock market. Founded on the principle that trading shouldn't cost you a fortune in fees, it lets you buy fractional shares of thousands of stocks and ETFs for zero commission—something that would have seemed impossible a decade ago.

The app democratizes retail investing by making it accessible, transparent, and genuinely affordable. While traditional brokers buried fees in spreads and commissions, Freetrade charges nothing for trades and offers a refreshingly straightforward pricing model. You get real-time data, a clean mobile interface, and the ability to build diversified portfolios without watching fees erode returns.

In a European market where retail investing was often treated as a luxury product for the wealthy, Freetrade positioned itself as the alternative—serious investing without the pretense or the price tag. The platform appeals to younger investors who want to own individual stocks and ETFs but were previously priced out or intimidated by legacy brokers.

Today, Freetrade represents a shift in how Europeans think about stock ownership: not as something reserved for the financially elite, but as a fundamental right. It's embedded itself in the broader fintech movement toward dematerializing finance and making capital markets participation the default rather than the exception.

Categories

Wealth

0

upvotes