Country

Companies10 of 77

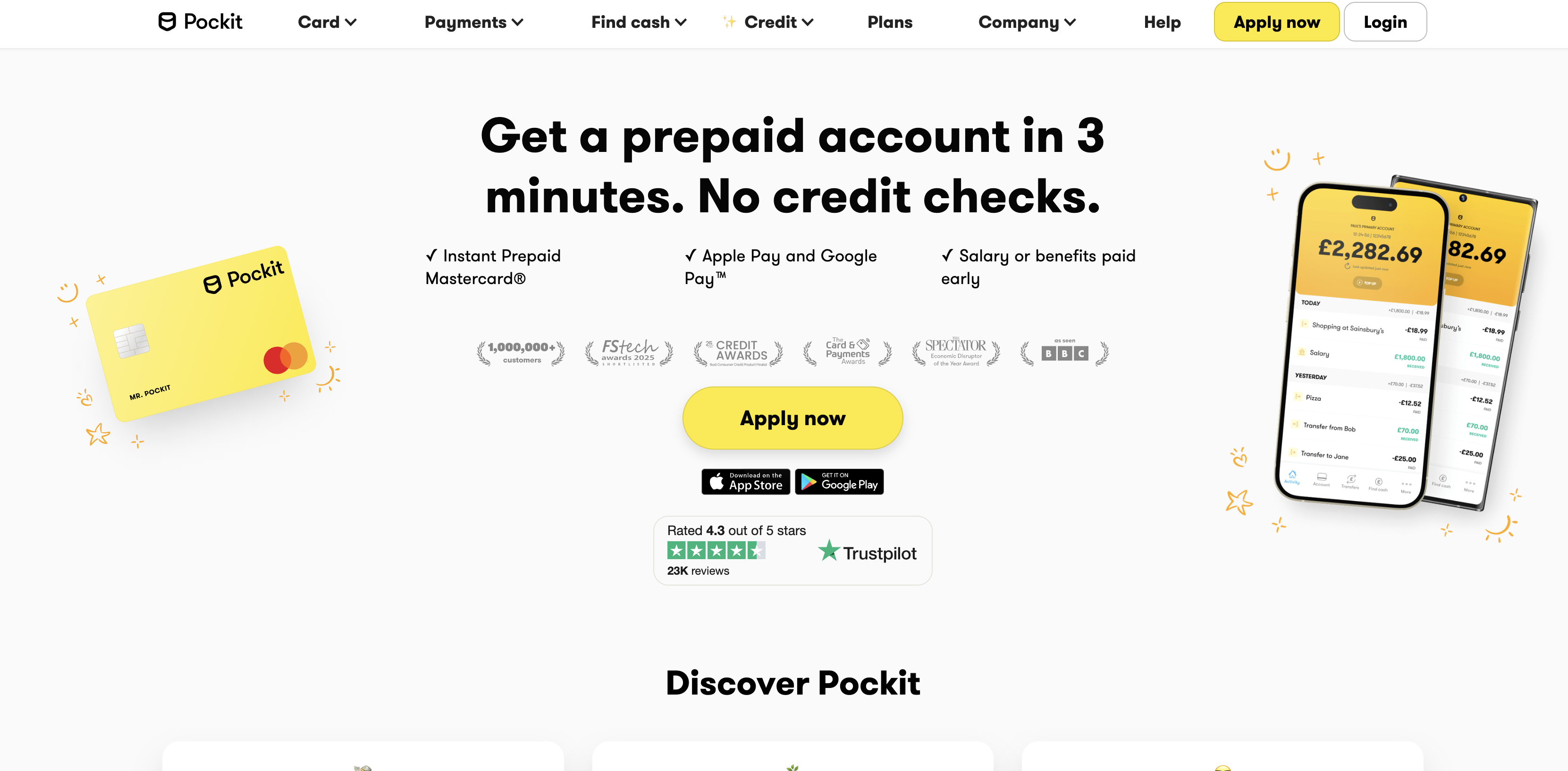

pockit.com

Pockit

pockit.com🇬🇧 United Kingdom

Pockit is a mobile-first financial platform designed for people who've been locked out of traditional banking. Rather than chasing the affluent, Pockit focuses on the underbanked—those without access to a current account, credit history, or the documentation banks demand. The app serves as a genuine alternative to brick-and-mortar banking, offering digital accounts, card payments, and money management tools entirely through your phone.

What sets Pockit apart is its commitment to financial inclusion without the gatekeeping. You don't need a credit score or payslip to open an account. Instead, the platform builds trust through usage patterns and behavioral data, creating pathways for people traditionally rejected by high street banks. This shifts the relationship from one of suspicion to one of genuine access.

The company operates across the UK and Europe, proving that underserved segments aren't just a niche—they're a substantial market. Pockit's mission is radical in its simplicity: banking shouldn't require jumping through hoops or having the right background. It's a challenger in the truest sense, not because it offers flashy features, but because it solves a real problem for millions of people who simply want to participate in the financial system.

Categories

Digital BankingPersonal Finance

1

upvotes

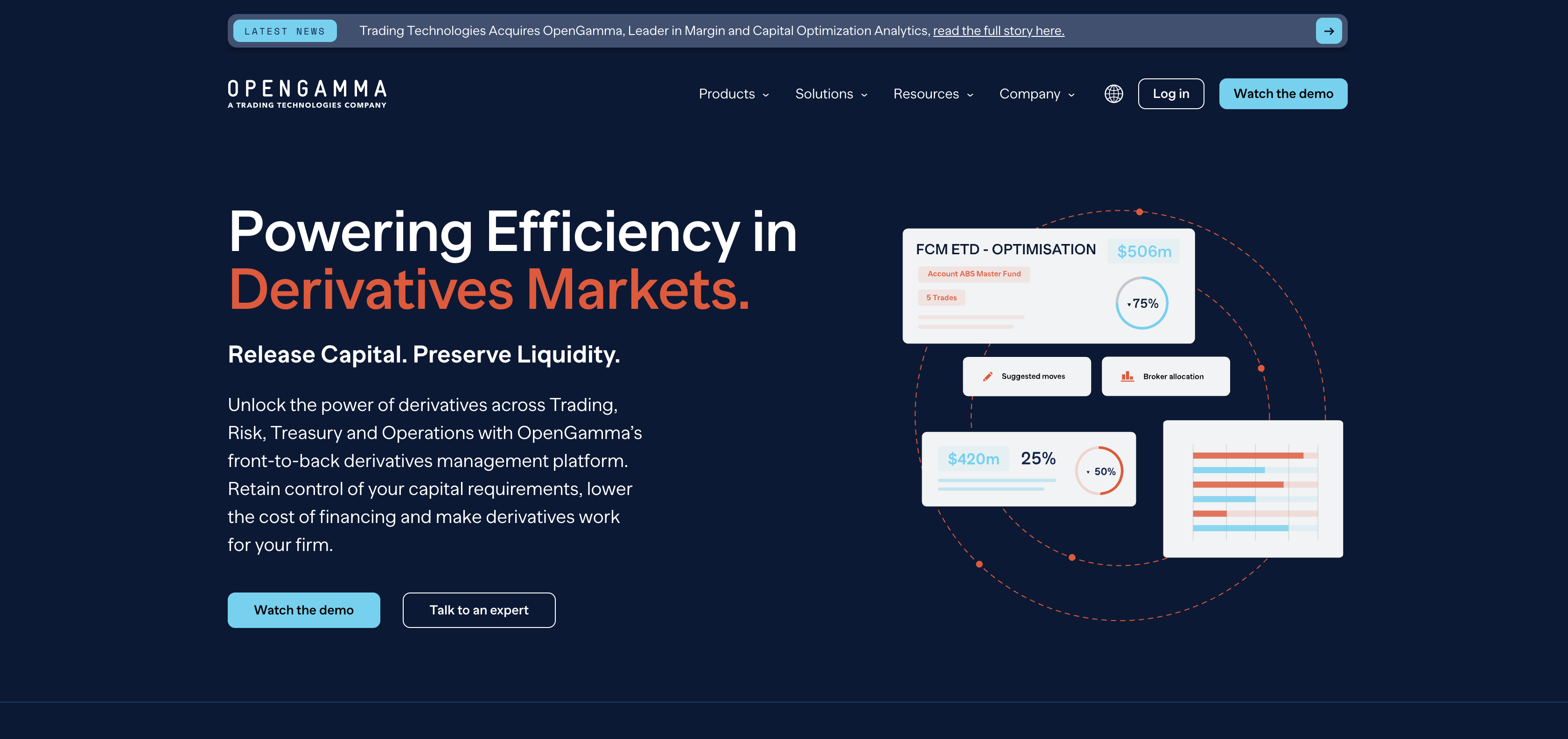

opengamma.com

OpenGamma

opengamma.com🇬🇧 United Kingdom

OpenGamma builds the computational backbone for how financial institutions price, value, and manage complex derivatives and fixed-income securities. In a world where legacy risk systems still demand custom Excel spreadsheets and manual reconciliation, OpenGamma delivers cloud-native valuation and risk analytics that run at scale—processing millions of trades in real time without the infrastructure headaches.

The platform combines market data ingestion, advanced pricing models, and scenario analysis into a single integrated stack. Banks and asset managers use it to replace fragmented point solutions, cut operational risk, and accelerate the pace at which they can launch new products. Think of it as the plumbing beneath modern capital markets trading desks: invisible, but critical.

OpenGamma's strength lies in its technical depth. The company targets sophisticated buy-side and sell-side institutions that need institutional-grade accuracy and auditability—not merely dashboards for non-experts. It competes against entrenched in-house systems and specialized vendors by offering flexibility and speed of deployment that rivals neither legacy providers nor lightweight startups can match.

In Europe's push toward regulatory standardization and operational resilience, OpenGamma has positioned itself as infrastructure for the next generation of risk management, where transparency, speed, and compliance are no longer separate concerns but engineered into the same platform.

Categories

Capital MarketsFinancial Infrastructure

0

upvotes

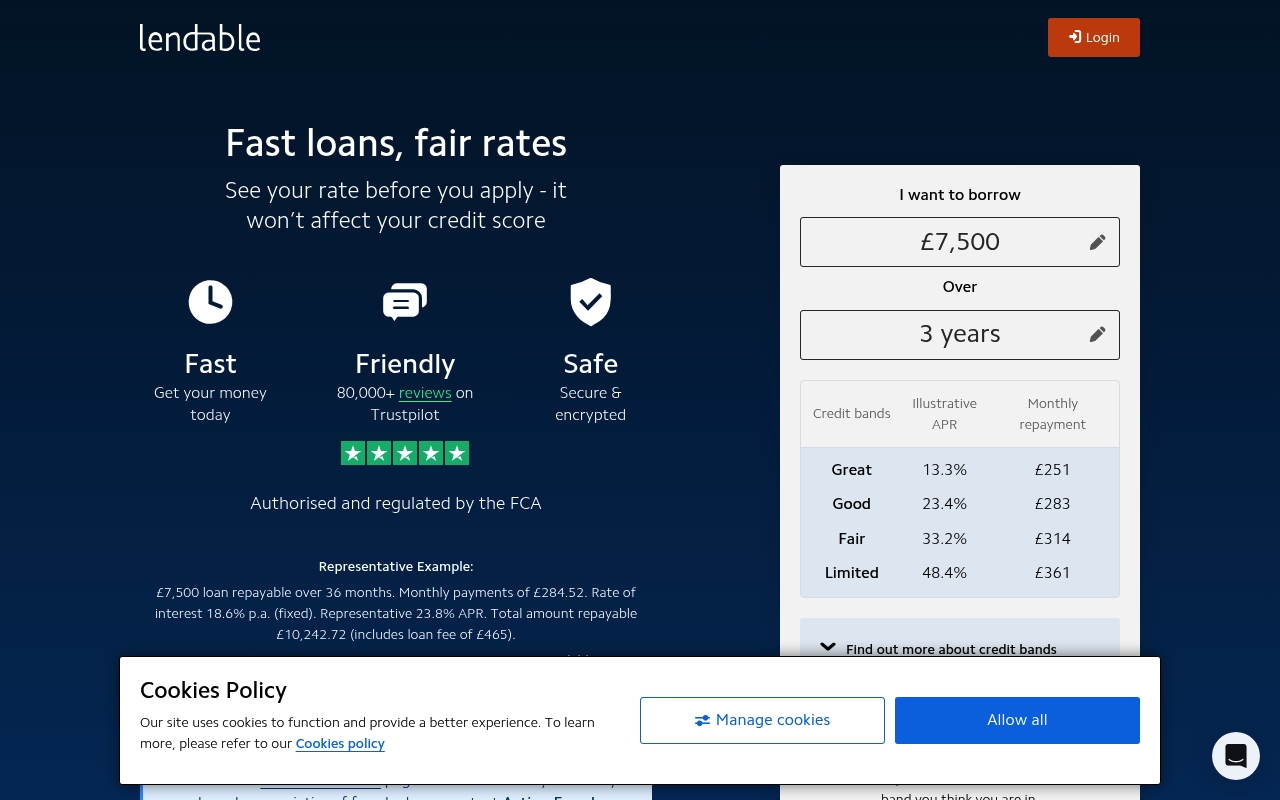

lendable.co.uk

Lendable

lendable.co.uk🇬🇧 United Kingdom

Lendable sits at the intersection of institutional finance and algorithmic credit. It's a platform that connects alternative lenders—think peer-to-peer platforms, fintechs, and non-bank lenders—with institutional capital markets. Rather than originating loans itself, Lendable acts as a market infrastructure layer, securitizing consumer and SME loan portfolios and selling them to institutional investors hungry for yield in an era of low rates.

The company essentially democratized access to capital markets for non-traditional lenders. Before Lendable, a mid-sized P2P lender or online SME lender couldn't easily tap into the deep-pocketed institutional buyers that banks routinely access. Lendable changed that by building the plumbing—origination APIs, portfolio management tools, and securitization infrastructure—that lets alternative lenders scale without warehousing risk on their own balance sheets.

In the European fintech landscape, Lendable represents a specific but growing category: the infrastructure play that enables other fintechs to thrive. It's not a consumer app; it's the backbone that lets consumer-facing lenders actually fund their ambitions. The platform has processed billions in loan assets and works with some of Europe's most recognizable fintech names.

Lendable's role in the broader ecosystem is that of a bridge—connecting the new world of distributed lending with the old world of institutional capital. It's quietly important infrastructure, the kind of thing that doesn't grab headlines but fundamentally reshapes how credit flows.

Categories

LendingFinancial InfrastructureCapital Markets

0

upvotes

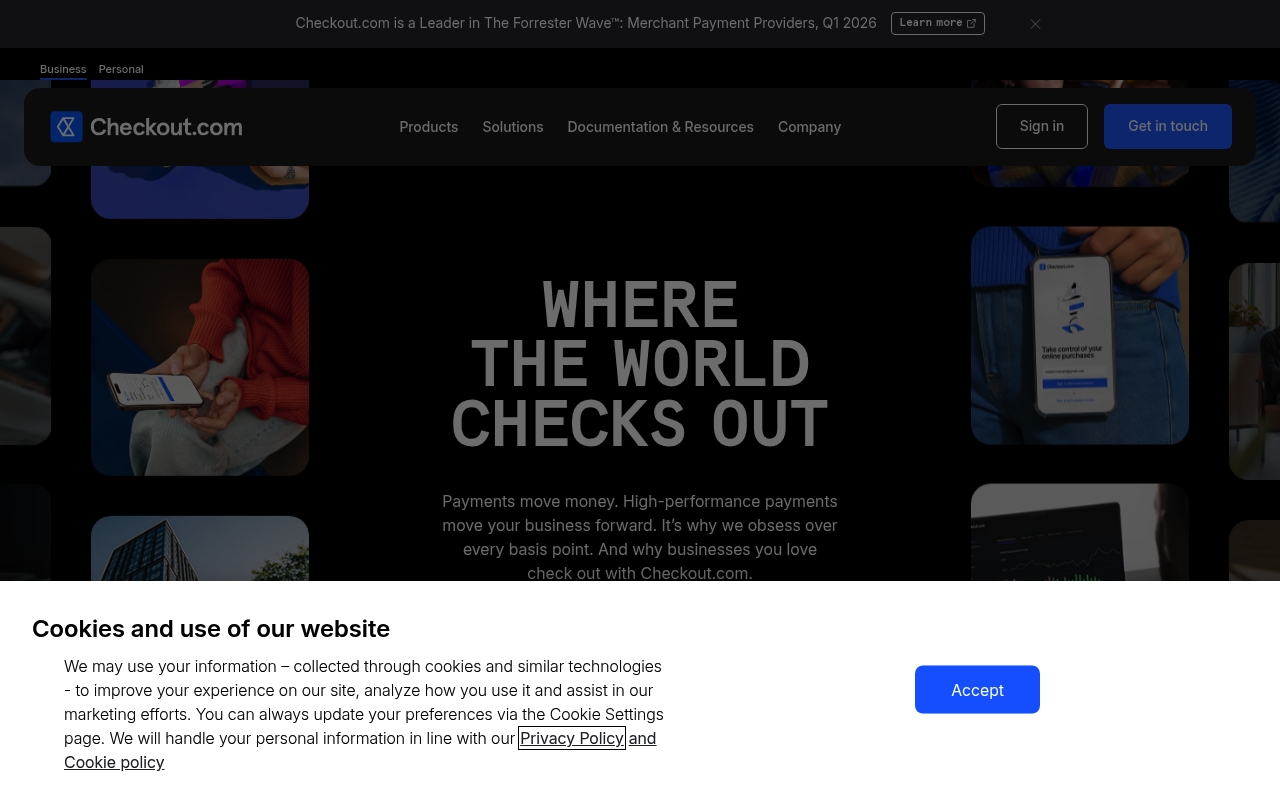

checkout.com

Checkout.com

checkout.com🇬🇧 United Kingdom

Checkout.com is a global payments infrastructure company that builds the plumbing beneath the surface of e-commerce. While most payment processors still operate like legacy banking rails, Checkout.com has constructed a single API that connects directly to card networks, acquiring banks, and alternative payment methods—eliminating the middlemen that slow everything down. The platform processes payments in over 150 currencies across 195 countries, handling everything from straightforward card transactions to complex multi-currency settlements for merchants operating at scale.

What sets it apart in Europe and beyond is its refusal to be a typical payment gateway: instead of asking merchants to adapt to the network, Checkout.com adapts the network to the merchant. Founded in 2012 by Guillermo Gutiérrez García-Ceballos, the company has grown from a London-based startup into a critical piece of infrastructure for enterprises, fintechs, and marketplaces that need orchestration at the transaction level. It competes with traditional acquirers and modern payment platforms by combining the reliability of legacy banking with the speed and flexibility developers expect.

In the fragmented European payments landscape, Checkout.com has become indispensable for companies that refuse to compromise on latency, coverage, or control. The company represents a fundamental shift in how payments should work: less about choosing between payment methods and more about making payments invisible.

Categories

PaymentsFinancial InfrastructureEmbedded Finance

0

upvotes

fundingcircle.com

Funding Circle

fundingcircle.com🇬🇧 United Kingdom

Funding Circle sits at the intersection of institutional capital and small business ambition. The platform connects SMEs with investors—funds, banks, and individuals—who want returns tied to real economic activity rather than abstract asset classes. It's fundamentally a marketplace, but one that's spent years learning how to assess credit risk at scale, price loans competitively, and move money across borders without the friction traditional finance demands.

The company operates across multiple geographies, though Europe remains central to its strategy. It handles everything from loan origination and underwriting through to servicing and portfolio management, meaning it's built real infrastructure rather than just matching borrowers to lenders. This matters because it allows institutional investors to actually understand what they're funding.

Funding Circle competes in a space where traditional banks have historically been absent—the mid-market lending gap where a £50,000 loan isn't big enough for a relationship manager but too important for a business to ignore. Alternative lenders have crowded this space, but Funding Circle's institutional backing and regulatory maturity give it a structural advantage. It's moved from pure peer-to-peer model toward a more hybrid approach, partnering with regulated lenders to expand reach while maintaining its marketplace credibility.

The company represents a fundamental rethinking of how capital reaches productive SMEs—not through gatekeepers, but through platforms that make risk transparent and pricing efficient.

Categories

LendingSME Finance

0

upvotes

creditspring.co.uk

Credit Spring

creditspring.co.uk🇬🇧 United Kingdom

Credit Spring is a UK-based fintech that treats financial distress like a health problem—one that deserves diagnosis and treatment, not judgment. Rather than simply offering credit, the company combines short-term loans with financial coaching and debt management tools, recognizing that a quick cash injection without context is often a band-aid on a bigger problem. The platform helps borrowers understand their spending patterns and rebuild their financial foundation, not just patch a temporary shortfall. It's a provocative stance in a market crowded with BNPL and payday lenders that rarely ask why someone needs money in the first place. Credit Spring targets people in the credit-vulnerable segment—those with poor or limited credit histories who'd normally be shut out of mainstream lending. Instead of algorithmic rejection, the company uses alternative data and behavioral insights to assess creditworthiness beyond traditional scoring. For users, this means faster access to reasonable credit at transparent rates. For the market, it signals a shift toward lending that acknowledges financial fragility as a temporary state, not a permanent condition. The company represents a broader move within fintech to attach financial wellness services to credit products, treating lending as an entry point to deeper financial health rather than a transaction.

Categories

LendingPersonal Finance

0

upvotes

payhip.com

Payhip

payhip.com🇬🇧 United Kingdom

Payhip lets creators and small businesses sell directly to their audience without the usual gatekeeping. It's a all-in-one commerce platform that handles digital products, physical goods, subscriptions, and memberships—essentially a Shopify alternative built for creators who want simplicity and fair pricing.

The platform lives in that sweet spot between marketplace and self-hosted store. You upload your product, set your price, share a link, and start selling. No approval process, no middleman deciding what you can or can't do. Payhip takes a percentage of each sale rather than charging upfront fees, which resonates with bootstrapped creators and solopreneurs who don't have predictable revenue yet.

What sets Payhip apart is its lightness. While traditional payment processors demand integration work and setup headaches, Payhip is deliberately frictionless—you can be live within minutes. It also gives sellers control over their own affiliate networks and customer relationships, something most platforms charge extra for or restrict.

In the crowded world of creator monetization tools, Payhip occupies the pragmatic middle: more powerful than a simple payment link, simpler than a full ecommerce platform, and designed specifically for people who want to sell without becoming a software engineer. It's quietly influential in how independent creators think about direct sales.

Categories

Embedded FinancePayments

0

upvotes

iongroup.com

ION Group

iongroup.com🇬🇧 United Kingdom

ION Group is a sprawling financial software empire that has quietly become one of Europe's most comprehensive infrastructure plays. The company operates across trading, risk management, and post-trade processing—the unsexy but absolutely critical backbone that powers global capital markets. Unlike flashy fintech startups chasing consumer adoption, ION builds the invisible plumbing that institutional traders, hedge funds, and investment banks depend on every single day. Its portfolio spans front-office platforms, market data aggregation, clearing and settlement systems, and regulatory reporting tools. ION serves as a counterweight to the purely consumer-focused fintech narrative, proving there's enormous value in solving problems for professionals who move billions. The company's strength lies in its ability to connect disparate financial systems, providing what amounts to a unified operating system for institutional finance. For European financial institutions, ION represents a trusted partner in an increasingly complex regulatory landscape, offering solutions that integrate seamlessly with legacy infrastructure while modernizing workflows. Its acquisition-driven growth strategy—picking up niche specialists and consolidating them into a cohesive platform—mirrors the broader consolidation happening across enterprise fintech. ION's market position underscores a fundamental truth about fintech: the biggest opportunities often lie in B2B infrastructure rather than consumer apps.

Categories

Capital MarketsFinancial InfrastructureRegTechTreasury

0

upvotes

moonpay.com

MoonPay

moonpay.com🇬🇧 United Kingdom

MoonPay sits at the intersection of crypto and traditional finance, offering on and off-ramps that let people move money between their bank account and crypto wallets with minimal friction. Founded in 2018, the London-based company has quietly become one of Europe's most important infrastructure plays in the emerging crypto economy, handling billions in transactions across more than 150 countries.

What sets MoonPay apart is its unglamorous but essential positioning: it's not trying to be a crypto exchange or a trading platform. Instead, it's the plumbing layer that makes crypto accessible to ordinary people. You buy crypto through MoonPay the same way you'd buy a digital service—seamless, compliant, and fast. The company operates with full EU regulation, holding licenses across multiple jurisdictions while maintaining the kind of compliance rigor that traditional banks expect. MoonPay's API-first approach means startups, wallets, and even traditional fintech apps can embed crypto purchasing directly into their user experience. This white-label capability has attracted partnerships with everyone from music platforms to gaming studios. The company has raised substantial funding and is valued at over a billion dollars, a testament to how critical crypto infrastructure has become. In a market obsessed with trading speculation and yield farming, MoonPay represents something more fundamental: the normalization of crypto as a payment asset class. It's doing for cryptocurrency what Stripe did for online payments—removing the technical and regulatory barriers that kept it confined to specialists.

Categories

Crypto & BlockchainEmbedded Finance

0

upvotes

freetrade.io

Freetrade

freetrade.io🇬🇧 United Kingdom

Freetrade is a London-based investing app that stripped away the gatekeepers between everyday Europeans and the stock market. Founded on the principle that trading shouldn't cost you a fortune in fees, it lets you buy fractional shares of thousands of stocks and ETFs for zero commission—something that would have seemed impossible a decade ago.

The app democratizes retail investing by making it accessible, transparent, and genuinely affordable. While traditional brokers buried fees in spreads and commissions, Freetrade charges nothing for trades and offers a refreshingly straightforward pricing model. You get real-time data, a clean mobile interface, and the ability to build diversified portfolios without watching fees erode returns.

In a European market where retail investing was often treated as a luxury product for the wealthy, Freetrade positioned itself as the alternative—serious investing without the pretense or the price tag. The platform appeals to younger investors who want to own individual stocks and ETFs but were previously priced out or intimidated by legacy brokers.

Today, Freetrade represents a shift in how Europeans think about stock ownership: not as something reserved for the financially elite, but as a fundamental right. It's embedded itself in the broader fintech movement toward dematerializing finance and making capital markets participation the default rather than the exception.

Categories

Wealth

0

upvotes